The 10 Steps To Solve Your Budget Troubles

Virtually every nonprofit struggles to balance its budget. Attempts to bring it into balance usually involve some combination of cutting expenses (often sacrificing future growth), and stretching the fundraising goal past the point of confidence. But it doesn't have to be that way.

About a year ago, I attended a workshop session at the University of Richmond's Institute on Philanthropy. Wally Stettinius, a statesman of the Richmond philanthropic community, led the session.Wally is a published author, the former Chairman and CEO of Cadmus Communications Corp., a faculty member at both the Darden School of Business (University of Virginia) and the VCU School of Business, disciple of Peter Drucker, and a go-to resource for area nonprofits.In his session, Wally presented a relatively simple but insightful tool -- a management accounting report that reorganizes the conventional budget format to shed light on both program costs and fundraising costs. It doesn't change the underlying format of how your Board-adopted budget should be organized -- it's simply an analysis tool to help you understand some key points about your nonprofit's finances.

Virtually everything in this post is credited to Wally.

Looking at Your Budget From a New Perspective

I'll explain the full process, but a broad overview could be divided into two categories: (1) turn your budget upside down, and (2) view fundraising costs as a factor of the amount of money needed to raise.

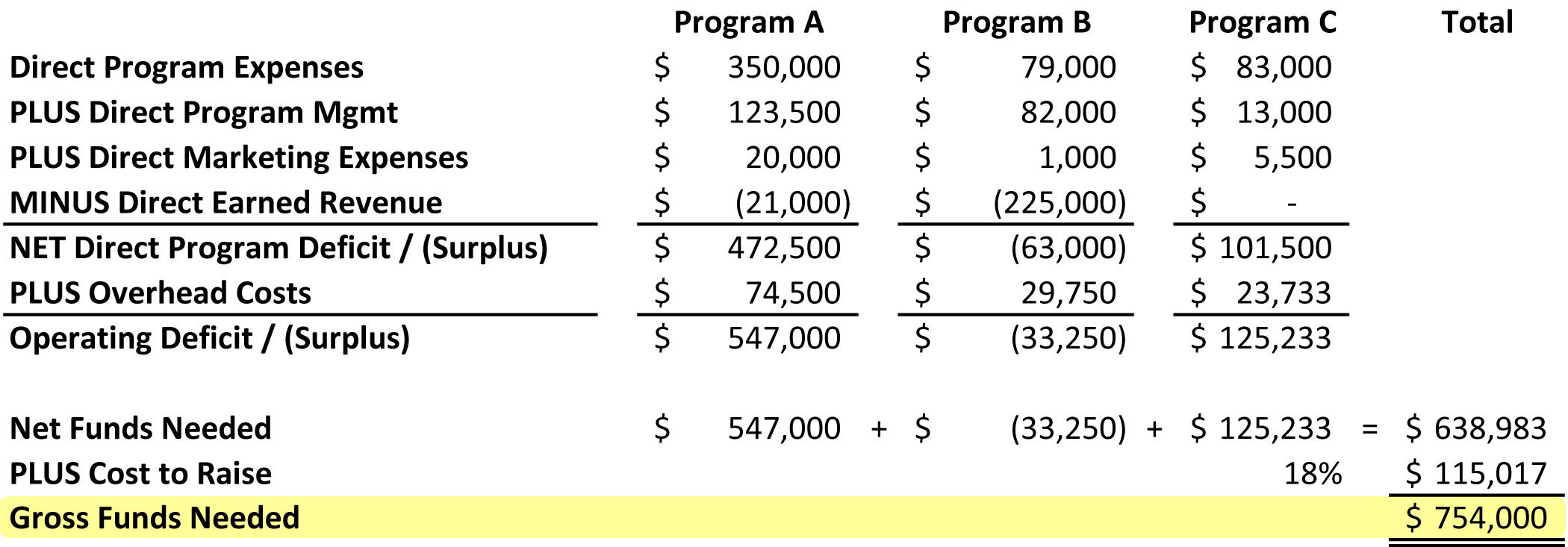

To keep things simple, the examples shown throughout are built on a hypothetical $1 million budget.

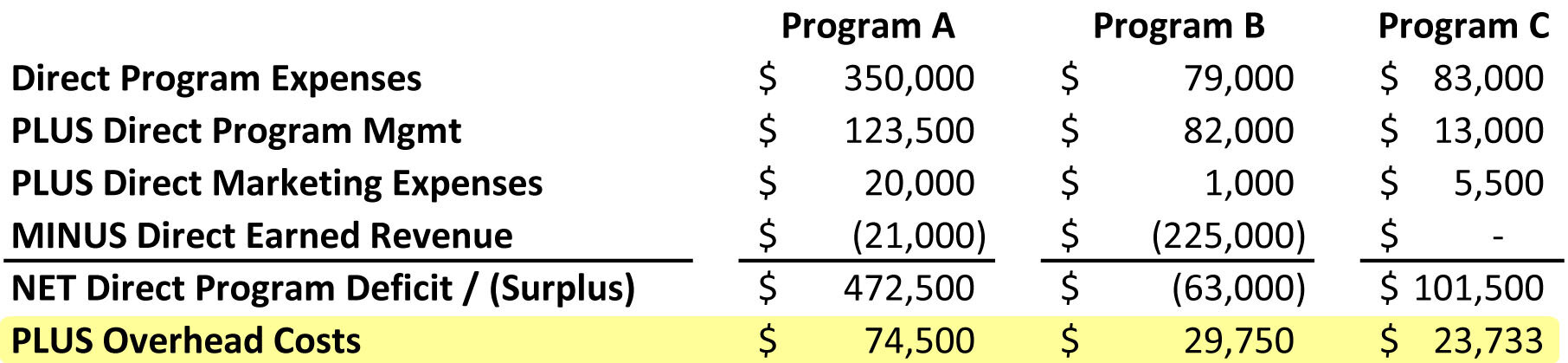

Step 1: List your direct expenses by program.

Take each program of your organization, and list its direct expenses at the top of each column. This includes the salaries/wages of program staff, supplies, rent, and other direct costs of running the program.

Step 2: List the direct management expenses for each program.

For any staff that spend time directly involved in or administering programs, you should include the portion of their salary applicable to each program (e.g. the Program Director's salary might be split proportionally between your three programs).

Step 3: List the direct marketing expenses for each program.

Think through both the obvious, direct marketing expenses, as well as any those that promote your organization as a whole. Divide the latter into programs proportionally, if needed.

Step 4: List your earned revenue.

Show the amount of earned revenue that you plan for each program. (As a reminder, earned revenue is income generated by the sale of goods or services, like ticket sales, tuition, registration fees, etc.) Some programs might have a significant amount, while others may have none.You're going to subtract this, so enter it as a negative number.

Step 5: Calculate the net direct program deficit (or surplus) for each program.

Total all rows so far to find the deficit/surplus for each program. Some programs might show a negative number -- good for you! This means that, at least on the basis of direct expenses and revenues, this program is profitable (contributes to your overhead), an unfortunately rare occurrence in the nonprofit field.

Step 6: List overhead costs.

Split your administrative overhead into the program columns according to whatever method your organization allocates it. Don't include any fundraising costs here -- just general administrative expenses (non-program staff, office rent, office supplies, utilities, etc.).

Unless you have exact figures based on analysis of each program, you can simply allocate this overhead according to the size of each program. Divide each program's total direct expenses by the sum total of all direct program expenses to get each program's percentage.

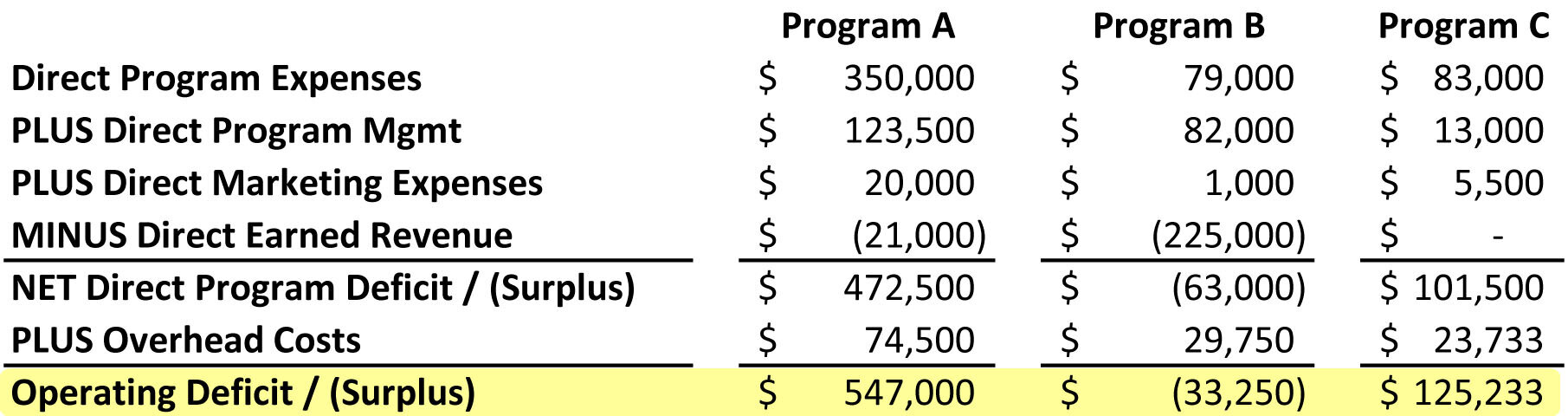

Step 7: Calculate the operating deficit (or surplus).

Add the overhead costs to the direct program deficit (or surplus). This shows the operating deficit (or surplus), which is the total amount of money that must be raised for each program.

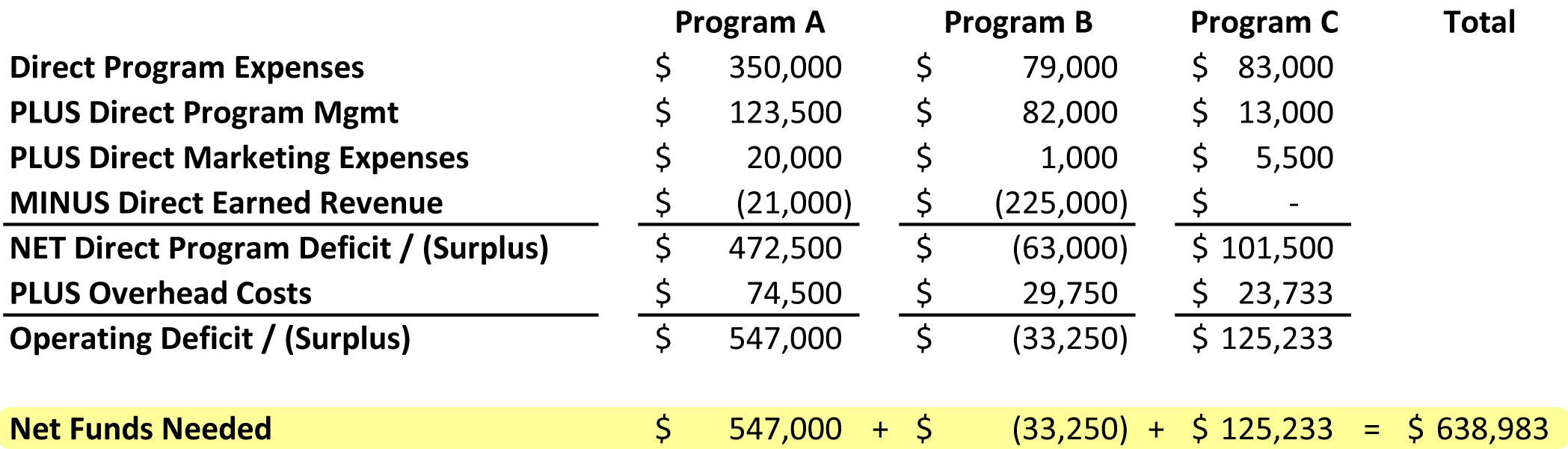

Step 8: Total the amount of contributed revenue needed.

Copy the operating deficits/surpluses into a new row called Net Funds Needed. Sum the net funds needed row into a new total to the right -- the contributed revenue needed to fund your operations. Note that any negative numbers are reducing the amount of money your team needs to raise (hooray for programs that pay for themselves!).

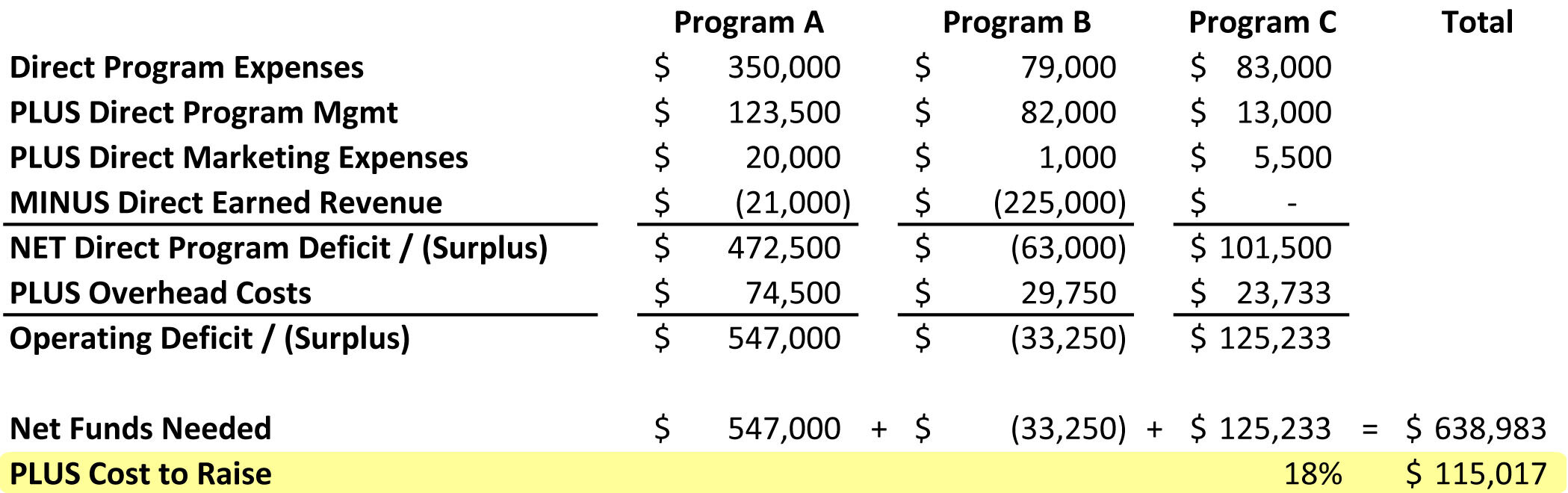

Step 9: Calculate the cost to raise.

Underneath that total, calculate the percentage you should plan to spend to raise it. For a stable nonprofit, this would be approximately 15%. For a nonprofit investing in sizable growth, it could be 20%. There is no hard-and-fast rule, but be thoughtful about this.

NOTE: The cost to raise does not equate to your "fundraising percentage." This oft-cited figure is calculated in reverse -- the amount of money spent on raising money, divided by the total amount raised. This percentage will turn out lower than the percentage you apply in this step.

Step 10: Calculate the total to raise.

Add the cost to raise to the contributed revenue needed. In other words, your total fundraising must cover both the contributed revenue needed for your programs, as well as the cost to raise it.

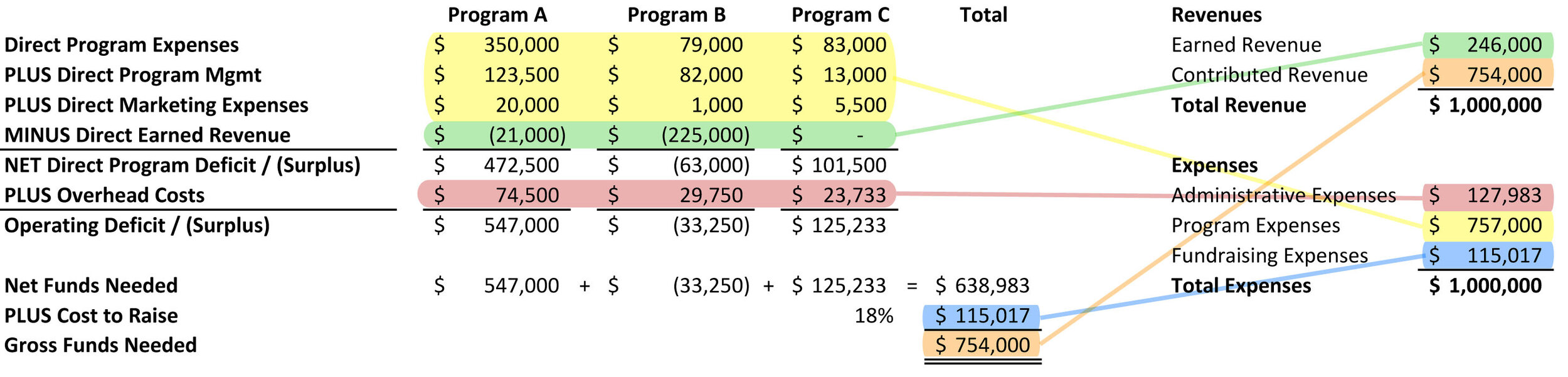

How does this relate to the conventional budget?

To see how all of this translates into a conventional (GAAP) budget format, click here.

Here's why this makes sense:

Fundraising Has Predictable Costs

In the for-profit sector, the "cost to raise" would be called a "selling cost" -- the amount of money it will take in marketing and distribution to sell the desired amount of goods or services. Of course, in nonprofit we would never use this term... right?!?!... so we'll call it "cost to raise.

"The calculated "cost to raise" shows how much you should be spending in your development activities. This includes the salary and benefits for any development staff (and/or the allocated salary and benefits for other positions partially engaged in solicitation, like the executive director). It also includes the printing, postage, events, and other costs associated with cultivation, solicitation, and stewardship.If your actual spending is below the amount of this calculation, then don't pat yourself on the back. You're not being efficient and frugal. You're under-investing, and you're depriving your organization of additional funding, both now and in the years to come.

Similarly, if you want to boost the amount of money you plan to raise, this tool will help you identify how much to spend to raise it. I know this may come as a shock, but just raising the goal without adding resources isn't likely to work.

Analyzing the budget in this way helps you avoid a critical mistake when the first draft of the budget doesn't balance: we slash anything we can, including development expenses. However, unless you are overspending on development, cutting down the development budget means also cutting into the contributions you'll likely receive this year and in the future. So by segregating the development budget to an area "below the line," you can focus your energies on the expense and income targets that will actually bring your budget into balance.

Final Thoughts

As nonprofit leaders, it is critical that we plan the work, then work the plan. The budget is the first step along this road. Getting a better handle on the real costs and funding needs of our programs is both enlightening and, if you're like me, refreshing. Wally's model does exactly that. Furthermore, segregating our fundraising costs from the nickel-and-dime game we play to balance our budgets helps to ensure that budgetary pressures don't become a self-defeating cycle.

I challenge you to set aside an hour and analyze your current budget using this model. I think you'll be surprised what you find!

I'd be happy to help, if you'd like to try this with your organization and need a hand.